By Sunil Subramaniam, Financial Sector Veteran & Ex-MD of Sundaram Mutual Fund, Chennai

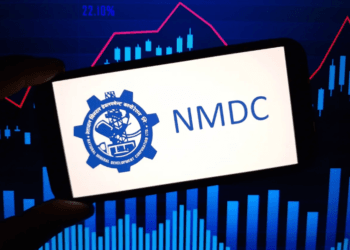

Both HDFC Bank and ICICI Bank represent roughly 25-30% of the Indian private credit market, making their results a direct proxy for India’s macro health.

Hence, this comparison is, in a way, a snapshot of the country’s financial health as of April 2026.

The attached image gives a snapshot of the two banks’ performance from this perspective

Key highlights

• SME Momentum: The high growth in business banking and SME books (17-20%) indicates that the manufacturing and industrial supply chains are the current engines of the “real” economy

• Credit/Deposit Mismatch: The core economic signal is the widening gap between credit demand (~12-16%) and deposit growth (~11-14%).

The banking system is probably effectively acting as a liquidity drain, which will keep real interest rates for borrowers elevated even in a neutral policy environment.

• Asset Hygiene: The clean NPA figures (~1.15-1.4%) show that There is no evidence of a systemic “stress” or a “debt bubble” despite higher interest rates and global geopolitical volatility.

Indian corporate sector is thus entering this phase of the cycle with incredibly low leverage, providing a solid floor for the macro outlook.

• The “Savings Shift”: The lag in deposit growth isn’t just a bank problem; it’s an economic indicator. It confirms that Indian household savings are shifting into capital markets, forcing banks to keep interest rates high to compete for cash.

• Rural Engine: ICICI’s 25.6% rural growth suggests a definitive turn in the hinterland economy, which should provide a significant floor for GDP growth in the coming quarters.

• The Consumption Pivot: The high growth in ICICI’s rural book and HDFC’s SME book suggests the economy is shifting from a “premium urban consumption” model to a “broad-based manufacturing/rural” model.

In summary, this data suggests the Indian economy is in a steady-state expansion phase, characterized by clean balance sheets and strong internal demand, but constrained by a tightening liquidity environment.

About the author:

Sunil Subramaniam, Former Managing Director and CEO of Sundaram Mutual Fund, is among the most seasoned voices in India’s investment management industry, with a career spanning over four decades across banking, insurance, and asset management. Currently, he advises several investment firms and financial institutions on macroeconomic trends, market strategy and asset allocation among others. He also runs a YouTube channel, ‘Sense and Simplicity by Sunil’, where he breaks down complex market trends, macroeconomic developments, and investment strategies into accessible insights for retail investors.

(Disclaimer: The views expressed are those of the author. Please consult your financial advisor before investing in stocks.)

{kind=link}