By Sunil Subramaniam, Financial Sector Veteran & Ex-MD of Sundaram Mutual Fund, Chennai

SIP TO BLAME FOR FIIs SELLING, RUPEE SLIDE: JEFFERIES!

The above report by Jefferies has caused a lot of confusion in the market. This is an attempt to understand the same and present a contrary opinion.

The mechanism that Jefferies describes:

1. Strong SIP inflows (MFs, EPFO, NPS) create deep domestic liquidity.

2. FIIs, facing expensive valuations and better EM opportunities, sell into this liquidity.

3. FIIs convert rupees to dollars to repatriate funds → higher dollar demand → rupee depreciation.

4. Because domestic flows absorb selling, markets don’t crash, but the FX side bears the pressure.

5. Equity market-driven outflows accounted for $78 billion over the last two years.

6. Capital account surplus has fallen to ~0.5% of GDP in FY25–26, the lowest ever, vs. 2.6% over the prior 10 years.

7. The Balance of Payments (BoP) situation has been negative for the past two years, with another negative year expected.

My analysis and views

SIPs are not the root cause—they’re the conduit/mechanism enabling exit. The real drivers are

2. FII valuation concerns (Indian equities trading at a premium vs. EM peers)

3. India’s weight in the MSCI Emerging market index have been steadily coming down causing passive funds to reduce India allocation in the re-balancing process

4. As a result, Indian markets have been among the worst performing within the Emerging Markets and could have caused further pullouts by investors from India dedicated funds.

5. Higher US real rates have made overall EM assets less attractive).

6. Tariff/trade uncertainty: US-India trade deal lack of clarity affected export growth and FII sentiment.

7. Geopolitical risk of Middle East war and its impact on Brent Crude prices (Crude is India’s largest import bill and India imports 85-%+ of its crude requirement).

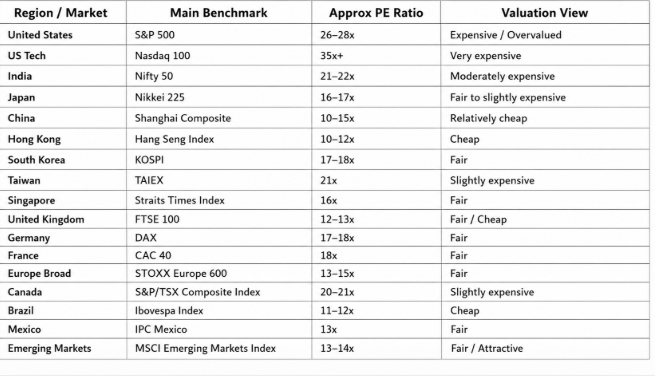

8. The Dedollarisation trend has driven Central Bank, Institutional and retail flows worldwide into precious metals such as Gold and Silver (Gold is India’s third largest import and almost wholly sourced overseas).See image

9. SIPs in fact, are stabilizing equity markets (preventing crashes) while FX absorbs the adjustment. Blaming SIPs wrongly equates the symptom with the cause.

10. RBI’s FX reserves and intervention strategies significantly affect rupee trajectory; this is largely omitted.

11. Jefferies says CAD isn’t the culprit, but, in my view, it is the expected widening of the CAD has compounded recent rupee pressure.

12. On the contrary If SIP growth slows, FIIs selling could lead to sharper corrections due to the impact of the lower domestic liquidity and lead to a domino effect of accelerating the outflows (to be the first ones to get out of the door!) domestic flows and could stress the rupee even further.

13. Further, the consistent SIP book has proven, in the light of consistent FII selling and consequent volatility in the Indian stock market, to be the best defense for long term retail investors as Rupee Cost Averaging as come into effect in full force and will ensure that the additional Mutual Fund units purchased during this period will be the best Wealth Creators in their journey towards achieving their future financial goals!!

The conclusion: This is a partially valid insight, but the narrative oversimplifies causality. SIPs are a stabilizer for equities, not the villain for the rupee.

About the author:

Sunil Subramaniam, Former Managing Director and CEO of Sundaram Mutual Fund, is among the most seasoned voices in India’s investment management industry, with a career spanning over four decades across banking, insurance, and asset management. Currently, he advises several investment firms and financial institutions on macroeconomic trends, market strategy and asset allocation among others. He also runs a YouTube channel, ‘Sense and Simplicity by Sunil’, where he breaks down complex market trends, macroeconomic developments, and investment strategies into accessible insights for retail investors.

Disclaimer: Any views, opinions, or investment-related information expressed by contributors on Databiztimes.com are solely their own and should not be construed as investment advice. Readers are advised to consult SEBI-registered or certified financial advisors before making any investment decisions.

{kind=link}