DBT Bureau

Pune, 20 May 2026

According to the latest Kedia Advisory Report, sugar prices remained resilient with gains of over 2.5% in the past month, supported by tightening global supply expectations, stronger ethanol demand, and improving bullish sentiment across major producing regions.

Highlights:

● Sugar prices gained over 2.50% monthly amid tightening global supply expectations.

● Government increased sugarcane FRP to ₹365 per quintal for 2026-27 season.

● India’s ethanol blending program diverted 3.1 million tonnes sugar equivalent supplies.

● Brent crude near $110 strengthened biofuel demand and sugar market sentiment.

● White sugar premiums remained firm amid tightening global refining capacity constraints.

● Citi expects global sugar prices rising toward 17 cents within three months.

● ISO projects global sugar market shifting into deficit during 2026-27 season.

● StoneX forecasts global sugar deficit after surplus during previous marketing season.

● El Niño concerns threaten Indian monsoon and future sugarcane yield prospects.

● Thailand forecasts 16% decline in sugar production amid lower cultivated acreage.

● Lower European sugar beet acreage continues supporting global white sugar prices.

● Brazil’s sugar output projected slightly lower during upcoming 2026-27 production season.

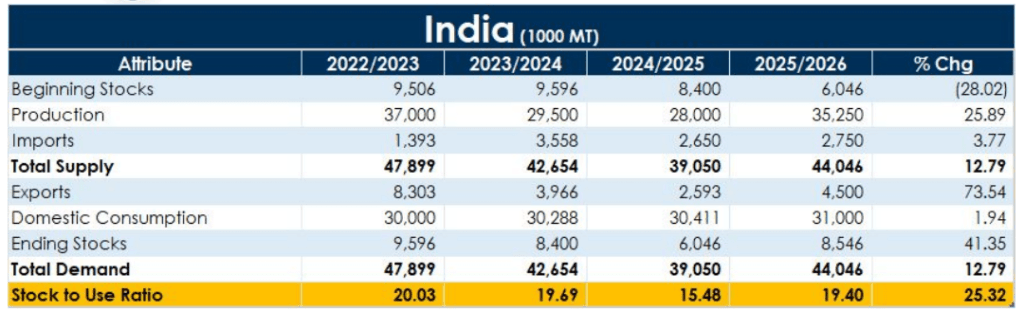

● India’s sugar production increased 7% yearly to 275.28 lakh tonnes recently.

● Brazilian sugarcane crushing surged 20% during April, improving near-term global supplies.

● India’s closing sugar stocks remain comfortable at 5.6 million tonnes currently.

● Government extended sugar export restrictions to ensure adequate domestic market availability.

● USDA projects India’s sugar market returning to surplus after two years.

Strengths:

● Sugar prices gained over 2.50% in a month amid supply concerns and Global sugar market to switch to a supply deficit as crops shrink.

● Sugarcane FRP for 2026-27 increased to 365 rupees per quintal, raising the floor cost.

● India’s ethanol blending target of 18% diverts 3.1 million metric tonnes of sugar equivalent.

● Geopolitical tensions in West Asia pushed Brent Crude to $110, supporting biofuels.

● White sugar premiums remain firm at 447.80 dollars per tonne due to refining constraints.

● Citi says it is bullish on sugar, sees prices rising to 17 cents in 3 months

Weaknesses

● India’s net sugar production surged 7% YoY to 275.28 lakh tonnes by April end.

● Brazilian sugarcane crushing in Center-South jumped 20% to reach 19.5 million tonnes in April.

● Ongoing LPG supply disruptions have indirectly slowed growth in commercial food outlet sugar consumption.

● Rapid closure of 121 mills in Uttar Pradesh signals a faster-than-expected seasonal supply peak.

● India’s closing stock of 5.6mmt ensures two months of domestic supply.

● ICE sugar speculators raised net short position by 6,637 contracts to 109,085 -CFTC

Opportunities

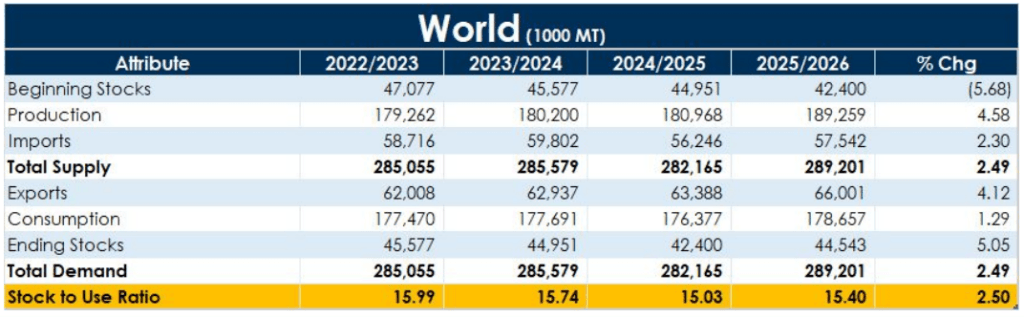

● The International Sugar Organization (ISO) expects the global sugar market to flip to a deficit of 0.262 million metric tons in 2026/27

● Global sugar market is projected to switch from a surplus of 2.29 million metric tons in the 2025/26 season to a deficit of 0.55 million tons in 2026/27 – StoneX

● El Niño threats raise concerns for Indian monsoon and 2027-28 sugar yields

● Shifting Indian demand toward “Clean Skies” aviation fuel creates a massive new ethanol market.

● Thailand forecasts 16% drop in sugar production for 2026-27 amid area contraction

● Lower EU sugar beet acreage of 8% creates a deficit that supports white sugar.

● Conab, reported that 2026/27 Brazil sugar output will decline by -0.5% to 43,952 MT

Threats

● Union govt has banned the export of sugar till Sept 30 this year with immediate effect, a move aimed at enhancing domestic availability

● USDA said it expects a 2026/27 sugar surplus in India by 2.5 MMT, the first surplus in two years.

● China reduced sugar import forecasts by 556,000 tons amid stricter syrup and premix controls.

● Increased distillation of grain-based ethanol could reduce the need for sugarcane-based fuel blending.

● To prevent price shocks, sugar mills must now strictly file monthly returns declaring physical stock levels to match digital ledgers.

FAO Sugar Price Index:

FAO Sugar Price Index averaged 88.5 points in April, declining 4.7% from March and 21.2% yearly. Expectations of ample global sugar supplies heavily pressured international sugar prices during the current marketing season.

Improved sugar production prospects in China and Thailand strengthened overall Asian supply outlook and market sentiment.

Favorable weather conditions supported crop development and boosted harvest expectations across key global producing regions. Brazil’s southern sugar-producing regions began fresh harvesting activities, increasing near-term exportable sugar availability globally.

Rising supply availability and improved harvest prospects collectively contributed to continued weakness in international sugar prices.

Conclusion:

Price Performance: Sugar prices gained over 2.50% monthly amid tightening global supply expectations and firm white sugar premiums. Sentiment remained supported by Brent crude near $110, which strengthened ethanol-linked demand. However, gains were capped by India’s sugar production rising 7% YoY to 275.28 lakh tonnes and Brazil’s sugarcane crushing increasing 20% during April, improving near-term supplies.

Ethanol & Policy Support: Government support remained constructive as sugarcane FRP for 2026-27 was increased to ₹365 per quintal, raising the production floor cost. India’s ethanol blending program diverted 3.1 million tonnes of sugar equivalent supplies, tightening domestic availability. Additionally, export restrictions were extended till September 30 to ensure adequate domestic supply and stabilize internal market conditions.

Global Supply Dynamics: Global sugar fundamentals indicate tightening conditions as ISO projects a deficit of 0.262 million metric tonnes during 2026-27, while StoneX forecasts a 0.55 million tonnes deficit after the previous surplus season. Thailand expects a 16% decline in production, and EU sugar beet acreage is down 8%. However, Brazil’s 2026-27 sugar output remains substantial at 43.952 MMT.

Stocks & Demand Outlook: India’s closing sugar stocks remain comfortable at 5.6 MMT, ensuring nearly two months of domestic supply availability. USDA expects India’s sugar market returning to a 2.5 MMT surplus during 2026-27 after two years. Additionally, China reduced sugar import forecasts by 556,000 tonnes, while higher crude oil prices risk slowing global economic activity and weakening sugar demand growth.

Technical Outlook: Technically, sugar prices continue holding firmly above the 3800 level, indicating sustained bullish momentum. RSI and MACD structures remain supportive, while volatility indicators suggest continuation of the prevailing uptrend.

Disclaimer:

Commodity investments are subject to market risks, including price volatility and economic uncertainties. Investors are advised to carefully read all related documents and assess their risk appetite before making any investment decisions. Past performance is not indicative of future results.

{kind=link}