DBT Bureau

Pune, 31 Jan 2026

LIC Housing Finance Ltd announced its unaudited results for the third quarter ended on December 31, 2025.

Performance highlights at a glance – Q3 FY2026

Performance highlights for the quarter ended December 31, 2025

Total disbursements were ₹16096 crs in Q3 FY2026 as against ₹15475 crs for the corresponding period in FY2025, up by 4%. Out of this, disbursement in the Individual Home Loan segment stood at ₹13094 crs against ₹12248 crs, up by 7% and the Non-Housing Individual Loan segment was at ₹2304 cr against ₹2094 crs, showing a growth of 10%, whereas project loans were ₹583 crs compared with ₹983 crs for the same quarter in the previous year.

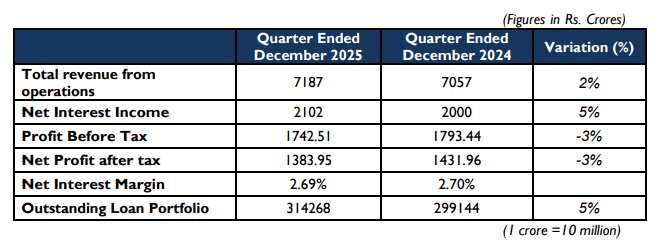

The Company’s Revenue from operations was ₹7187 crs as against ₹7057 crs, a growth of 2%.

Net Interest Income (NII) was ₹2102 crs, as against ₹2000 crs for the same period in the previous year, up by 5%. Net Profit after tax stood at ₹1383.95 crs compared with ₹1431.96 crs during the same period in the previous year. The Individual Home loan portfolio stood at ₹265890 crs as against ₹254652 crs, a growth of 4%. Project Loan portfolio stood at ₹8827 crs as on December 31, 2025, as against ₹8776 crs as on December 31, 2024. Total outstanding portfolio grew by 5% to ₹314268 crs from ₹299144 crs.

Net Interest Margin (NIM) for the quarter ended December 31, 2025, was 2.69% as against 2.70% in December 31, 2024, and 2.62% for September 30, 2025. Under IndAS 16, asset classification and provisioning changes for future credit loss are reported on an Expected Credit Loss (ECL) basis.

As per the same methodology, the provisions for ECL stood at ₹5105 crs as on December 31, 2025, with a coverage of 54%, as against ₹4974 crs as on December 31, 2024, and ₹5074 crs as on September 30, 2025. The stage 3 exposure at default as of December 31, 2025, stood at 2.45% as against 2.75% as on December 31, 2024, and 2.51 % as on September 30, 2025.

Performance Highlights at a glance – 9M FY2026

During the nine months ended December 31, 2025, the total disbursements for the company stood at ₹45525 crs against ₹44866 crs for the same period of the previous year. Out of this, the Individual home loan segment registered a disbursement of ₹37831 crs, as against Rs 36231 crs, up by 4% and the Non-Housing Individual loan segment registered a growth of 17% from ₹5384 crs to ₹6288 crs.

Total disbursements under project loans stood at ₹1117 crs as against ₹2901 crs for the nine months ended December 31, 2024.

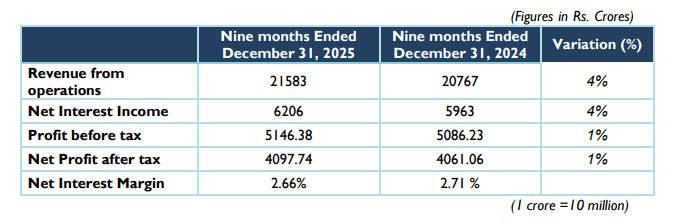

The Company’s Revenue from operations during this period was ₹21583 crs as against ₹20767 crs, up by 4%. Net Interest Income (NII) for nine months was ₹6206 crs as against ₹5963 crs during the same period of the previous financial year.

Profit before tax (PBT) for nine months in FY2026 was ₹5146.38 crs as against ₹5086.23 crs during the same period previous year. Net profit after tax for the nine months ended December 31, 2025, was ₹4097.74 crs as against ₹4061.06 crs during the same period previous year. Net Interest Margin (NIM) for the nine months ended December 31, 2025, stood at 2.66% as against 2.71% for the corresponding period ended December 31, 2024.

Speaking on the performance, Tribhuwan Adhikari, Managing Director & Chief Executive Officer of LIC Housing Finance Limited, said, “Our Q3 FY26 performance has been steady, with sequential improvement in both margins and asset quality. The reduction in borrowing cost has further supported margin expansion and the profitability of the Company. Looking ahead, we expect the forthcoming Union Budget to provide an additional boost to the housing sector, particularly across the affordable and mid-income segments, along with the continuance of thrust, which will support sustained demand and healthy credit growth. Traditionally, the January-March quarter has been a strong period for the housing finance industry, and we expect to close the financial year with good numbers.”

{kind=link}