By Sunil Subramaniam, Financial Sector Veteran & Ex-MD of Sundaram Mutual Fund, Chennai

June 2026: A classic game of two halves, where a major geopolitical pivot completely inverted the market’s trajectory, risk appetite, and positioning.

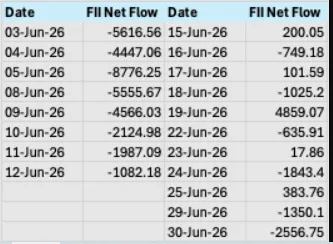

- Institutional Flows: From Risk-Off Havoc to Confident Re-Entry

The institutional narrative underwent a complete regime shift mid-month as geopolitical friction gave way to diplomatic breakthrough.

First Half (The Escalation Phase): Caught in the teeth of the US-Israel-Iran geopolitical conflict, FIIs engaged in aggressive risk-off liquidation. Rising energy costs and a hardening DXY led to heavy daily cash market outflows, which were absorbed by DIIs via consistent SIP mobilisation.

Second Half (The Ceasefire Capitulation): The announcement of the ceasefire completely altered the macro calculus. FII selling slowed to a crawl and turned into aggressive net buying on select days.

- Volatility Index (India VIX): The Textbook Mean Reversion

The India VIX provided a perfect visual map of the month’s psychological transformation.

First Half (The Anxiety Peak): As conflict escalation threatened shipping routes through the Strait of Hormuz, option premiums expanded rapidly. The India VIX climbed toward the 17.00–17.50 zone, reflecting genuine near-term hedging and fear.

Second Half (The Volatility Crush): The moment diplomatic breakthroughs and ceasefire agreements stabilized the geopolitical landscape, the risk premium dissolved. Brent crude retraced down to the $73–$74/bbl territory, triggering a massive volatility crush. The VIX collapsed sharply to close the month at 13.61, signalling a clean return to a stable market regime.

- F&O Derivatives Picture: From Bearish Pinned to Bullish Rollovers

The derivatives positioning underwent a structural migration across the June series expiry.

First Half (The Bear Grip): Early in the series, heavy Call writing at the 24,000 and 24,200 strikes acted as an insurmountable ceiling. The Put-Call Ratio (PCR) plummeted into oversold territory below 0.80, signalling aggressive hedging and short buildup.

Second Half (The Short-Squeeze Expiry): The geopolitical breakthrough caught call writers off guard. A fierce short-squeeze kicked off in the final week, forcing call unwinding and driving the index toward its milestones. Put writers aggressively shifted their bases upward, building a fortress-like floor at 23,500 and 23,700. The PCR recovered to a highly constructive 0.95–1.05 range, and positions rolled over into the July series with long biases firmly established in large-cap banking and defensive sectors.

Short covering in index futures combined with fresh cash allocations saw institutional liquidity heavily reinforce the market’s bottom.

- Advance-Decline Ratios: How NIDI (Non Institutional Domestic Investors) reacted A Complete Breadth Inversion

The internal health of the market shifted from heavily degraded to robustly healthy.

First Half: During the pre-ceasefire drawdowns, the market breadth was overwhelmingly bearish, frequently skewing worse than 1:3 (Advances to Declines). Small-cap and micro-cap stocks bore the brunt of this generalized liquidity withdrawal.

Second Half: Following the ceasefire, the market breadth staged a dramatic U-turn. Advances completely dominated declines as beaten-down counters experienced sharp, high-volume relief rallies. The final weeks characterized a broad-based, healthy participation rather than a narrow, index-heavy move.

- Cap Curve & Sectoral Performance: From Defensive Hiding to Mile-High Milestones

The structural behaviour across capitalizations and sectors cleanly reflects this binary split.

First Half: The Flight to Safety

With Brent crude spiking, the initial market response was defensive. The broader indices corrected swiftly, with mid-cap and small-caps experiencing sharp drawdowns as retail sentiment wavered. Money hid in Pharma, Healthcare, and Metals (acting as commodities hedges), while the IT sector suffered painful multi-session losing streaks under the dual weight of global macro strain and structural AI headwinds.

Second Half: The Euphoria Surge & Milestone Breach

The ceasefire acted as a massive catalyst, removing the primary energy inflation threat overhang.

The 24,000 Milestone: Relief buying triggered a massive capital pivot back into high-beta and structural domestic plays. The Nifty 50 staged a roaring comeback, to settle the month at the brink of 24,000 (23,865.25).

The Banking Leadership: Banking and Financial services took the baton to lead the charge. Bank Nifty put up a stellar show.

The Broader Market Rebound: Mid-caps and small-caps recovered all their lost ground and more, turning early-month pain into a robust closing rally. Real Estate led the structural recovery (+1.31%), and even beaten-down Auto names found late-month operational comfort as crude concerns cooled.

About the author:

Sunil Subramaniam, Former Managing Director and CEO of Sundaram Mutual Fund, is among the most seasoned voices in India’s investment management industry, with a career spanning over four decades across banking, insurance, and asset management. Currently, he advises several investment firms and financial institutions on macroeconomic trends, market strategy and asset allocation among others. He also runs a YouTube channel, ‘Sense and Simplicity by Sunil’, where he breaks down complex market trends, macroeconomic developments, and investment strategies into accessible insights for retail investors.

Disclaimer: Any views, opinions, or investment-related information expressed by contributors on Databiztimes.com are solely their own and should not be construed as investment advice. Readers are advised to consult SEBI-registered or certified financial advisors before making any investment decisions.

{kind=link}